Extensive expertise allows SpenceDrake Tax Lawyers & Experts to devise effective solutions for individuals and businesses. Below are examples involving various Tax Law issues…

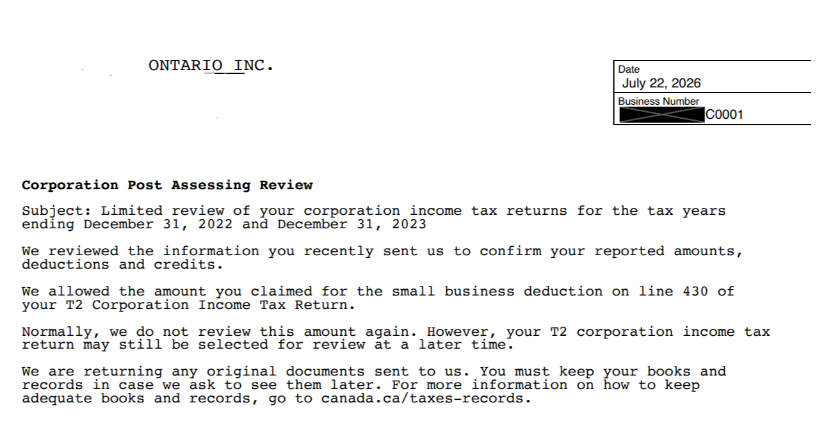

CRA reviewed a corporate client’s claim for the small business deduction upon the assumption it was earning passive and not active business income. We assisted with a written submission to CRA detailing the respective facts and law which was accepted by CRA in favour of our client.

A company conducting highly innovative work developing photonic systems and sensors had successfully claimed SR&ED credits for multiple years through one of the Big 4. The SR&ED funding was vital to their technological advancements. Yet, a claim for a particular year was subsequently reviewed and arbitrarily denied over very flimsy factual assumptions. One being that the work was conducted after the project was completed. Note, the project is still incomplete. Initially, only a portion of credits claimed, related to the work developing 10 of 30 prototypes tested at sites around North America, was allowed. According to CRA, the work for the remaining 20 prototypes did not qualify as SR&ED.

SR&ED Notices of Objection take a very long time for resolution, a couple of years is common in our experience. The previous representative filed an objection and we subsequently filed a Tax Court Appeal. Most importantly, considering the still incomplete multi-year project, eligibility was reversed from ineligible to eligible. As a result of our appeal, work related to the additional 20 prototypes was held to be SR&ED. Implicitly, CRA’s assumption that the project was complete when the work occurred was not supported by the facts, opening a path to continued project development.

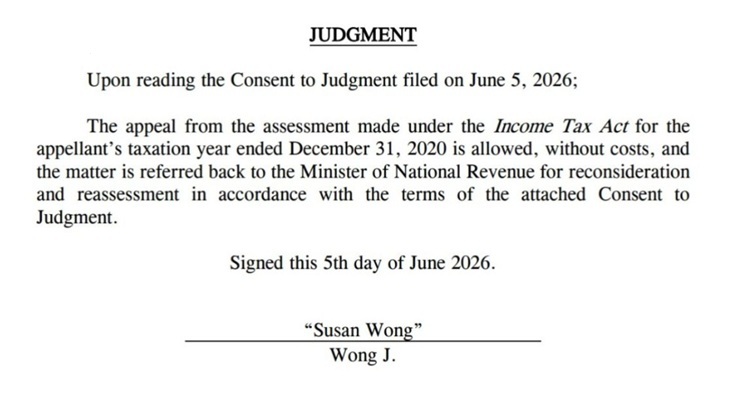

From the Consent to Judgement:

CRA conducted a Net Worth Audit of our client and his corporation. Taxable income was drastically increased leading to +$500,000 in additional corporate and personal income tax plus gross negligence penalties and interest reassessed as accruing since the statute-barred 2013 taxation year. The auditor’s incentivized corporate income tax reassessment resulted in the assumption that the individual received taxable shareholder benefits from the corporation, a common issue.

Their accountant was not able to reduce the reassessments. We filed Tax Court Appeals and were successful in establishing that the majority of the assumptions underlying the reassessments were incorrect. From one example of many, the auditor did not account for multiple corporate liabilities such as outstanding loans as well as available losses.

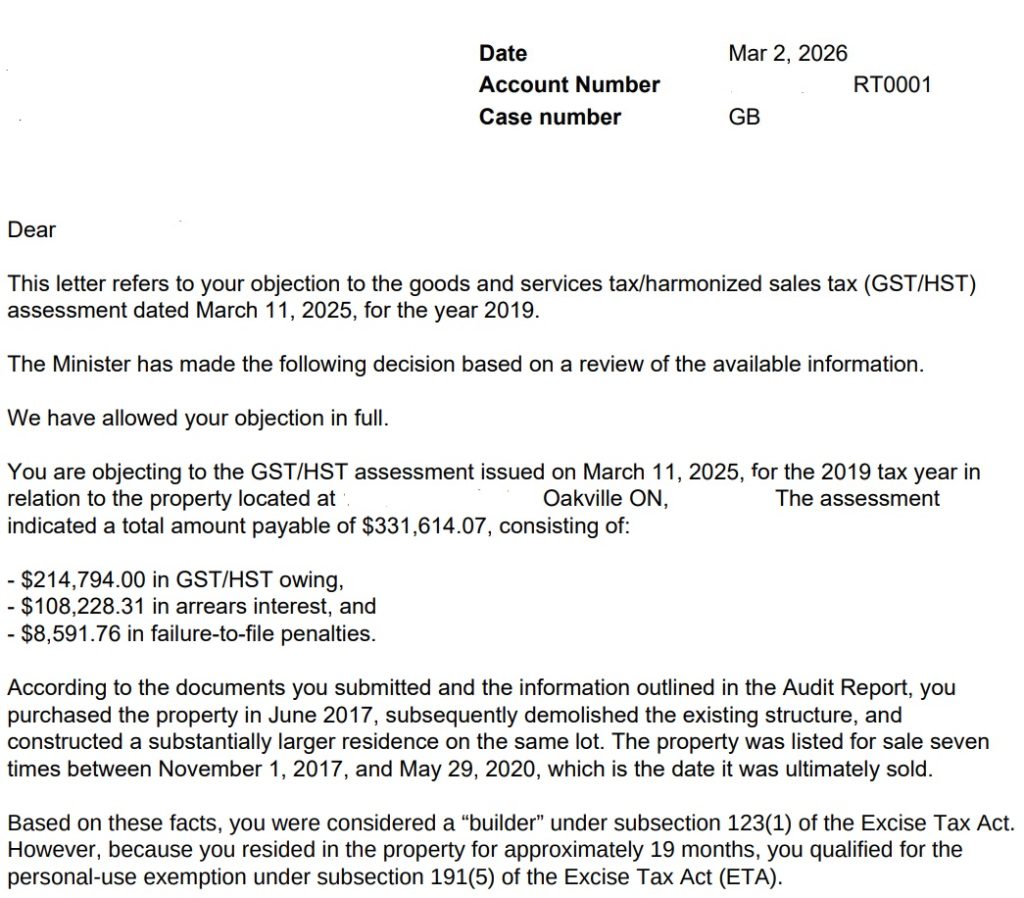

CRA has been targeting home sales. In some cases, even if a home is built to be a personal residence, CRA will assume the taxpayer was in the business of buying and selling homes and therefore should have charged and remitted GST/HST. Yet, there are many situations where a home is constructed or renovated by a taxpayer but then sold despite the intention of long-term residence. For example, a couple may split and sell the home as a result. In our experience, in the majority of cases CRA auditors will not give the taxpayer the benefit of the doubt and will assess hundreds of thousands of dollars in GST/HST. Importantly, as in this example, an exemption applies if the taxpayer resided in the home. Therefore, in addition to other considerations, proving residence can be key to avoiding a large punitive assessment.

It took multiple submissions to CRA appeals before available losses were applied reducing the majority of the assessed tax owing for our client.

During the Covid pandemic, businesses that require in-person patronage, such as restaurants and pubs, faced the challenge of paying for staff and business operations while also remitting trust amounts (e.g. CPP/EI & GST/HST) to the Canada Revenue Agency (CRA). Many had to switch to delivery only. Accordingly, by the end of the pandemic, businesses had large tax debts and some still do.

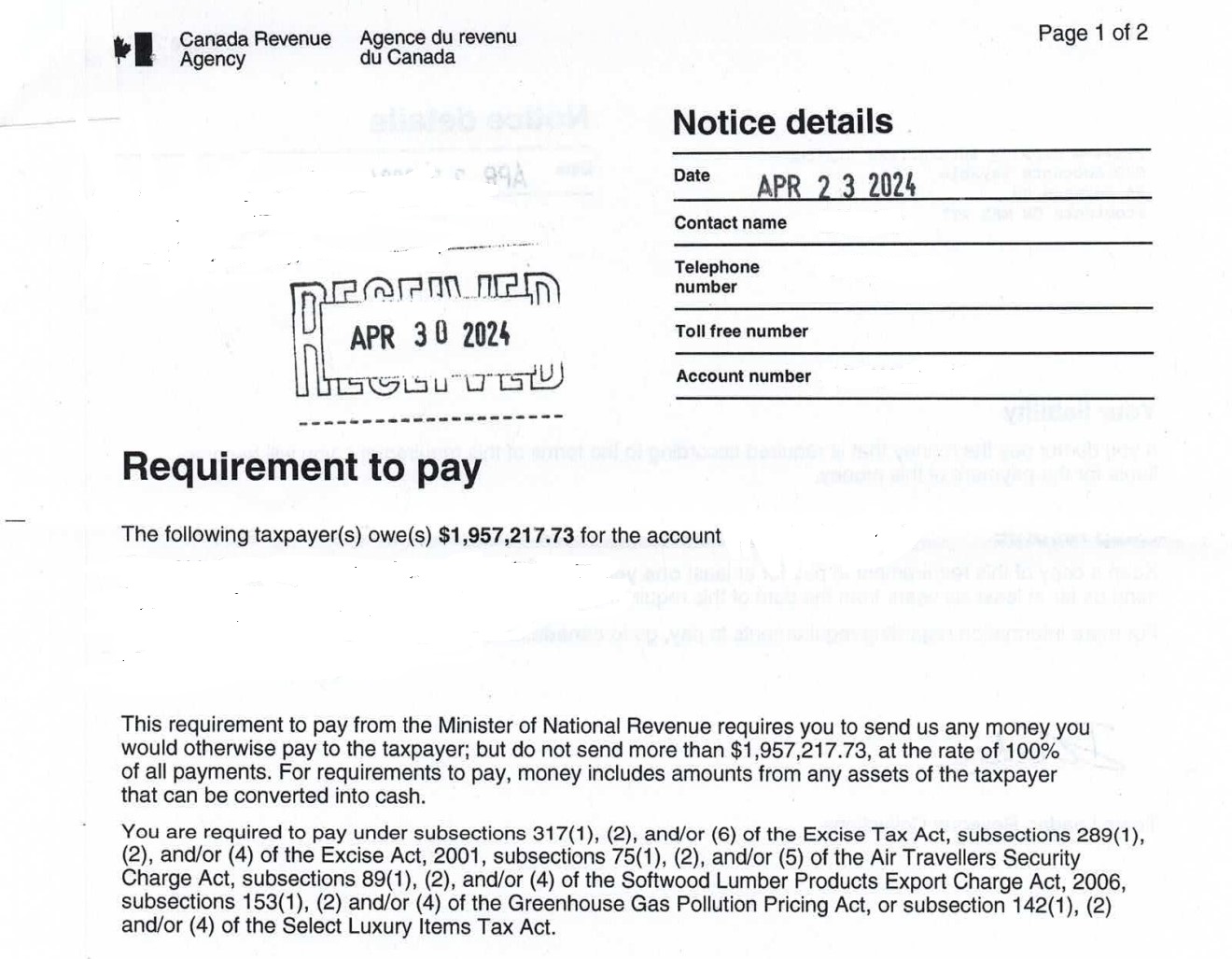

Under certain circumstances, CRA can force a third-party to pay the tax arrears of the indebted taxpayer. One way they can do so is by issuing a Requirement to Pay (RTP). In this case, CRA issued an RTP for over $1.9M to one of our client’s suppliers.

However, we were able to prevent the enforcement of the RTP by establishing that the factual relationship between our client and the third-party did not support the requirements necessary for CRA to execute the RTP.

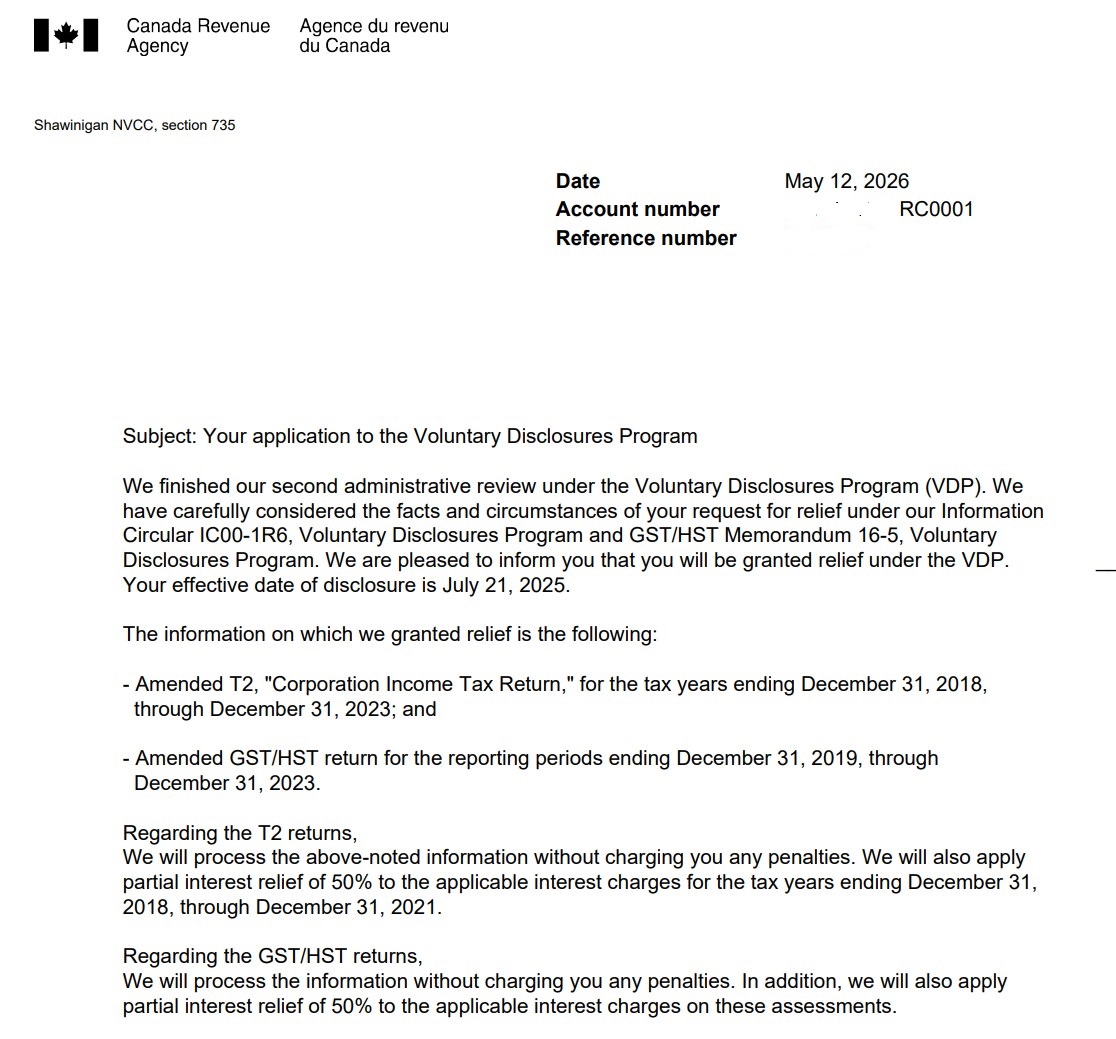

A taxpayer can submit a Voluntary Disclosure application to CRA to attempt to receive relief from interest and financial and criminal penalties for non-compliance. We submitted Voluntary Disclosures for an individual client’s 4 corporations related to approximately $1,000,000 in additional taxes. 3 of the 4 disclosures were initially denied based on a related audit. We then submitted detailed requests for a second administrative review with reasons disputing the initial denial including that the audit did not compel the taxpayers’ disclosures as well as establishing a breach of procedural fairness based on a unique set of facts.

Canada Revenue Agency (“CRA”), in this case along with Health Canada, regulate and enforce non-compliance with the Excise Act, 2001 (SC 2002, c 22), not to be confused with the Excise Tax Act (R.S.C., 1985, c. E-15).

The client came to us after CRA and Health Canada ruled that they were manufacturing vaping products without the required licenses and assessed approximately $3,500,000 in penalties, with accruing daily interest of course. In fact, the client does have a license and is a successful vaping business.

At the same time, CRA is auditing additional years and transactions for the client’s multiple corporations. Recently, for one of the multiple ongoing audits, we were able to prevent the assessment of a lower penalty for alleged Unpackaged Vaping Products.

A Notice of Objection was filed against four statute barred Notices of Reassessment resulting from a Net Worth Audit of an individual and related corporation. As a result of the Notice of Objection, the CRA appeals officer reduced the income inclusion of ~$500,000 in one particular taxation year by ~$250,000 along with the corresponding gross negligence penalties. The other years were all reduced but by lesser amounts. CRA also reduced the income of one of the corporation’s taxation years by ~$184K along with smaller reductions to the other two taxation years. In total, over a $600,000 income reduction by the CRA appeals officer. The taxpayer is appealing further to the Tax Court of Canada.

CRA has been targeting subcontractor expenses. A CRA auditor denied 100% of our client’s Input Tax Credits for GST/HST paid on subcontractor expenses and applied Gross Negligence Penalties. With a Notice of Objection we recovered $555,932.62 of $684,890.81 including removal of the Gross Negligence Penalties. With a second Notice of Objection we recovered approximately 90% of the outstanding Input Tax Credits.

CRA has been targeting subcontractor expenses. A CRA auditor denied 100% of our client’s Input Tax Credits for GST/HST paid on subcontractor expenses. With two Notices of Objection we recovered about 95% of the Input Tax Credits. Below is a result of the second Notice of Objection.

A Director of a corporation can be held personally liable for tax debts of a corporation under certain conditions. One being that a Director must be assessed within 2 years of resignation.

Our client, a student at the time, was listed as a director of a corporation that he had very little involvement with. Foreign persons paid him to complete the incorporation and prepare a website. After that he was not involved with the corporation and was not aware he was listed as a director nor the potential tax liability that attracted.

Years later, the corporation was assessed for over $10,000,000 in GST/HST and the legal collection notices were addressed to our client and the corporation. First, we had our client resign according to the statute imposed specifications.

We then made multiple written submissions to CRA supported by the facts, evidence and relevant law including that our client was at most a nominal director during the period the tax arrears accrued. Ultimately, CRA accepted our client’s position and he no longer faces the risk of personal liability for over $10,000,000 in GST/HST.

We filed a notice of objection on behalf of our client arguing that the Canada Revenue Agency’s audit decision was incorrect. CRA claimed our client had unreported cryptocurrency capital gains and assessed an extremely high gross negligence penalty. Our objection was allowed in full, with the removal of over $100,000 of capital gains and the deletion of a gross negligence penalty of over $375,000.

As a result of an audit, CRA readjusted the majority of our client’s filing position substantially increasing the tax owing. With a Tax Court Appeal we were able to reverse ~50% of CRA’s reassessments.

A United States Financial Technology (Fintech) corporation with $2B in assets sought a legal opinion on the tax implications related to a Canadian entity. Research was conducted accordingly and eventually we created and implemented the Canadian corporation.

Our client’s representative retained us to appeal the denial of medical expenses. With a Notice of Objection all expenses denied by the CRA Auditor were correctly allowed by the CRA Appeals Officer. Similar expenses being reviewed by CRA for a subsequent taxation year, in approximately the same amount, were also allowed.

The corporation conducted innovative work but a significant portion of their SR&ED tax credit claim was denied in this particular year. The client was technically advanced and handled the audit without representation. However, about 50% of their claim was denied after audit.

We were retained to appeal the SR&ED claim denial in the Tax Court of Canada. To do that we first filed a Notice of Objection and 90 days following we filed a Tax Court Appeal. We drafted and submitted highly technical pleadings and the appeal was settled early. In subsequent years, the client’s SR&ED tax credit claims were accepted as filed without audit.

The client, who resided in Europe but had lived in Canada for a period, failed to report Canadian source income for many years, including from multiple investments with a Canadian bank. He also received child tax benefits as a non-resident of Canada. We filed a detailed voluntary disclosure application and requested 90-days to file the requisite tax returns and a payment plan for the tax owing. The disclosure was accepted under the General program which ensured no financial penalties (50% of the tax owing) as well as no criminal penalties and partial interest relief for the tax owing.

A client’s successful business was subjected to a Net Worth Audit, which the Tax Court of Canada refers to as a “blunt instrument.”

The business accounting books and records were in poor shape and the client used bank accounts for both personal and business transactions, in significant amounts. The auditor reviewed the client’s records and bank accounts and decided to assume that all business income that flowed through a personal account was attributed directly to her. She reported $70,000 in income that year.

Nevertheless, CRA increased her personal income by over $2,600,000, relying on the assumption that all the funds that streamed in and out of a personal account were paid directly to her. Any experienced Tax Lawyer or Accountant will tell you that punitive inflated audit outcomes such as this are not uncommon, especially if the taxpayer is unrepresented.

A Tax Lawyer disputed the Net Worth Audit tax assessment. A Notice of Objection was filed in an effort to convince a CRA Appeals Officer that the auditor’s accounting was indefensible in court.

If the inflated assessment wasn’t appealed, the client would have lost her business due to CRA collections actions making it impossible for her to function (e.g. seizing bank accounts or operating lines of credit). Or she would have been forced into bankruptcy. Either way a successful business and jobs would have been destroyed for naught.